The GENIUS Act is an issuer-side law. AmLaw firms have been writing about it from that angle since July 2025: how Circle, Paxos, and Société Générale-Forge ramp to capital floors, how Tether's path looks, what the SEC carve-out means for tokenized money-market funds. That coverage answers the issuer's question. It doesn't answer yours.

If you're an app builder embedding USDC, PYUSD, or USD1 — fintech, neobank, remittance, marketplace, agentic spend — the GENIUS Act doesn't license you. It changes the perimeter around you. Issuer-side obligations cascade into distributor terms; distributor terms cascade into your KYC, sanctions, and policy stack. This is the integrator's map: what changes, when, and the 11 things you ship before the July 2028 cliff.

The five things the law actually does

GENIUS regulates payment stablecoins: USD-pegged tokens designed for payments rather than investment. The five core rules:

- 1:1 reserve backing in cash, repo-backed cash, insured deposits, or short-dated U.S. Treasuries. No fractional reserves. No commercial paper.

- Reserve attestation — quarterly attestation by a registered public accounting firm. Annual audited financial statements (PCAOB standards) for issuers above $50B in consolidated outstanding issuance.

- OFAC sanctions screening on mint and redeem. Issuer-side BSA/AML program with SAR filing.

- Redemption at par within statutory windows. No issuance gating that breaks redemption.

- No algorithmic stablecoins. Fiat-backed only for payment stablecoins. (Tokenized money-market funds remain in SEC scope.)

Around those rules, a federal/state dual track exists: state-chartered issuers below a federal-supervision threshold operate under state law; non-bank issuers above the threshold elevate to federal supervision (Federal Reserve / OCC, depending on charter). State-chartered "crypto banks" (Wyoming SPDI, NY Trust) continue as alternative routes.

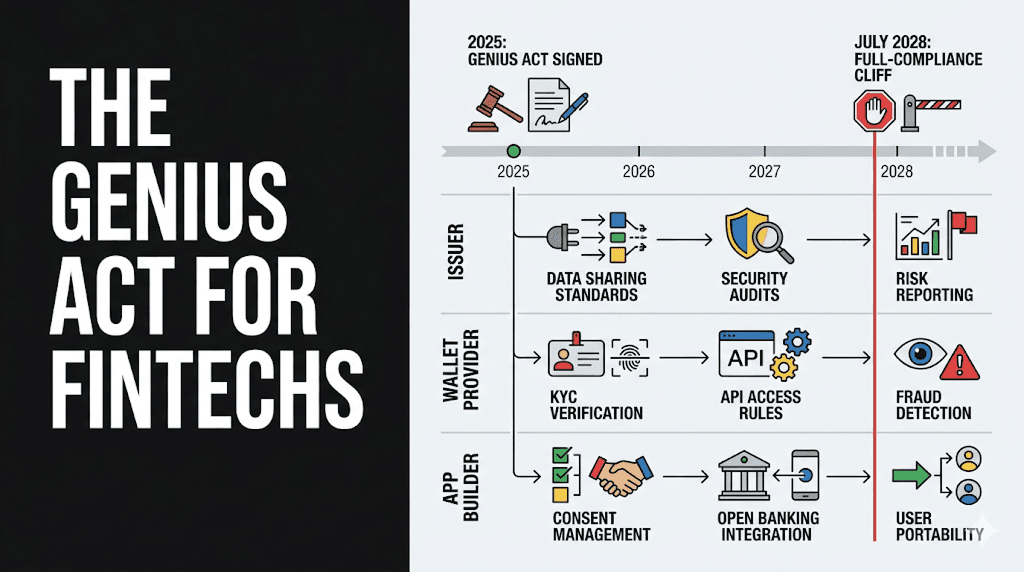

The cliff calendar — what moves when

| Date | Who moves | What changes |

|---|---|---|

| July 2025 | Issuers | Act signed. Transition rules begin. Existing issuers continue under prior state authorities while federal regime stands up. |

| Late 2025 → 2026 | Federal Reserve, OCC, FinCEN | Implementing regulations published. Reserve-composition rules, attestation cadence, BSA/AML program details finalised. |

| 2026 → 2027 | Issuers | Capital floor step-up phases in. Reserve composition tightens. Quarterly attestations become standard practice. |

| 2027 | Banks, credit unions, payment networks | Federally-regulated US rails begin distinguishing "qualified stablecoins" from non-compliant. |

| July 2028 | Everyone | Full-compliance cliff. Non-compliant payment stablecoins lose access to federally-regulated US rails. Issuer-side BSA programs at full effect. |

Builders treat the cliff as a date-anchored migration plan, not a single switch. Issuer-side communications throughout 2026–2027 will surface which tokens make the cut.

The integrator cascade — five paths from issuer to your app

GENIUS lands on issuers; obligations flow downstream through five channels. Each channel changes a different part of your stack.

1. Tightened distributor terms

Issuers (Circle, Paxos, SG-Forge) will tighten the terms by which wallet providers, exchanges, and processors distribute their tokens. Expect: enhanced KYB on distributors, stricter sanctions clauses, mandatory Travel Rule readiness, and faster timelines on suspicious-activity reporting.

Your impact: the wallet rails you embed will surface these terms as their own integration requirements. Pick a wallet provider that has the issuer-side relationships and the compliance posture to absorb them — not one you'll have to swap when distributor terms tighten.

2. Qualified-stablecoin scope

Federally-regulated US rails (bank fintech, credit unions, payment networks integrating stablecoins) will distinguish "qualified" payment stablecoins from the rest. Non-compliant tokens lose easy access to those rails.

Your impact: your policy engine needs an allow-list. USDC, PYUSD, USD1 today; the list evolves through 2027. Apps holding non-compliant balances will need rebalancing flows before 2028.

3. Sanctions screening cascade

GENIUS mandates OFAC screening at the issuer layer (mint/redeem) plus expects distributor-side screening on transfers. Wallet providers screen at signer init and pre-sign. Builders screen on user onboarding.

Your impact: sanctions screening on every outbound transfer is no longer optional — and the screening cadence (real-time vs daily refresh) matters. Wallet providers exposing a fail-closed pre-sign hook against a cached, periodically-refreshed sanctions list are the right shape.

4. Recordkeeping and reporting expectations

Issuer-side BSA programs produce audit trails. Distributors and wallet providers will need to surface matching records: who held what, when did they move it, at which KYC tier, with what sanctions-screen result.

Your impact: your audit log needs structured fields — user ID, KYC tier, sanctions-screen result, Travel Rule data, counterparty type — exportable for regulator letters and SOC2 controls.

5. Liability redistribution

When a wallet is compromised, when funds move to a sanctioned address, when a redemption fails — GENIUS sets the issuer-side liability bar. Distributor and integrator contracts will reflect that bar.

Your impact: your integration contracts with the wallet provider matter. Read the indemnity and liability clauses; understand which failure modes sit with you (KYC at onboarding, financial-promotions in your marketing) vs the wallet provider (signing-layer sanctions, Travel Rule plumbing) vs the issuer (mint/redeem AML).

The 11 things app builders ship before the cliff

The integrator-side compliance engineering minimum. Print this, tick it off.

- KYC at user onboarding. Vendor-agnostic interface. Tier 1 / 2 / 3 mapped to balance and behaviour. See Stablecoin KYC for Builders for the perimeter map.

- OFAC sanctions screening on every transfer. Pre-sign hook in the policy engine. Cached list, periodic refresh, fail closed.

- Travel Rule originator data plumbing. Wallet provider populates the fields from your bound KYC. Tested for the EU TFR (every transfer, no threshold) and US FinCEN ($3,000) thresholds.

- Qualified-stablecoin allow-list. Policy engine restricts the tokens your app routes by default. USDC, PYUSD, USD1 today — evolving.

- Tiered transfer limits. Daily, weekly, per-transaction caps tied to KYC tier and risk score. Enforced at signing.

- Redemption-window awareness. If you offer redemption to fiat, surface issuer-side cadence. Don't surprise users with a non-instant redeem when the issuer queues it.

- BSA/AML-aligned audit logging. Structured fields on every signed transaction; 5-year retention minimum.

- MSB registration (if US-domiciled and you transmit value above de-minimis). Most builders running backend wallets (server-signed flows) need this. Federal registration via FinCEN.

- State MTL stack (US users). Via direct filing in your home state plus an MTL-as-a-service partner (regulated payment institution that holds the broader stack) — or full-stack BitLicense if NY exposure is high.

- FinCEN SAR filing process. Internal escalation runbook; SAR-filing decision tree; counsel-approved template.

- Counsel-blessed BSA program (if you operate a backend wallet at scale, particularly for US users). Designate a BSA Compliance Officer, document the program, train staff, refresh annually.

For the role × jurisdiction matrix that covers GENIUS plus MiCA, FCA, MAS, and VARA, see Stablecoin Regulation and Licensing.

Issuer-by-issuer outlook (best read as of mid-2026)

| Issuer | Tokens | Likely path | Why |

|---|---|---|---|

| Circle | USDC, EURC | Federal route. Likely first to full GENIUS compliance. | Already publishing reserve attestations; bank-charter-style posture. |

| Paxos | USDP, PYUSD, USD1 | Federal route. PYUSD especially well positioned. | NY Trust charter background; PayPal partnership operationally mature. |

| Société Générale-Forge | EURCV (EUR-pegged, but US USD-pegged path possible) | Cross-Atlantic compliance. | EU-anchored issuer with US distribution ambitions. |

| Tether | USDT | Uncertain. Offshore issuer; may take partial-compliance + reduced-US-access path. | Reserve composition history; jurisdictional positioning. |

| Algorithmic stablecoins | DAI (partly), FRAX, others | Out of GENIUS scope. Either restructure to fiat-backed or remain non-payment-stablecoin. | GENIUS prohibits algorithmic payment stablecoins. |

| Bank-issued stablecoins | USDB (Stripe Bridge), bank consortium tokens | Federal route via bank chartering. | Bank-issued tokens have a clean GENIUS path. |

The practical builder takeaway: USDC, PYUSD, and USD1 are the safe defaults through the cliff. Hedge against issuer concentration with a multi-token strategy in the policy engine.

Where the wallet provider fits

The policy engine is where GENIUS cascades into code. A compliance-aware wallet rail exposes the hooks that make the 11-item list above shippable in weeks rather than quarters:

- KYC vendor adapter — bring Sumsub, Persona, Dotfile, or in-house. The wallet provider doesn't lock you in.

- Sanctions hook at signer init and pre-sign. Fail closed.

- Travel Rule plumbing — originator + beneficiary fields populated from bound KYC.

- Qualified-stablecoin policy — token allow-lists per wallet, per sub-account, per user tier.

- Tier-gated limits — daily, weekly, per-transaction caps tied to KYC tier.

- Audit log with structured fields for BSA/AML and SOC2 export.

Openfort's smart-account wallets expose these hooks directly. The regulated entity in the flow — your business — remains the policy enforcer. The wallet primitives do the load-bearing work; your compliance team writes JSON instead of email.

Common failure modes

- "The GENIUS Act is an issuer problem." It originates issuer-side. It cascades to you through distributor terms, qualified-stablecoin scope, and sanctions expectations. Plan for the cascade.

- "I'll wait until 2028 to react." Issuer-side communications and federally-regulated US rails will tighten through 2026–2027. Retrofit cost compounds with user-base size; ship the 11-item stack early.

- "I'll just stick with USDC and ignore the rest." USDC is a safe default, but multi-issuer support is risk management — concentration risk and chain-availability risk both matter.

- "My wallet provider handles compliance." They expose the hooks. You bring the KYC vendor, write the policies, file the SARs, and own the user perimeter.

- "I don't need MSB registration because I'm self-custodial." Self-custodial user wallets typically avoid CASP/MSB classification for those wallets. Backend wallets, custodial settlement layers, and any server-side signing for users put you back in MSB territory.

Conclusion

The GENIUS Act is a date-anchored migration plan for the entire US stablecoin stack. Issuers are the headline; integrators are the silent majority. The 11-item checklist above is the integrator's shipping list — wire it through your wallet provider's policy engine, not as a one-off compliance bolt-on.

For the global regulatory landscape (MiCA, FCA, MAS, VARA, GENIUS in one map), see Stablecoin Regulation and Licensing. For the user-perimeter view of KYC and sanctions, see Stablecoin KYC for Builders. For the payment-rails cost-and-speed view, see Stablecoin Payment Rails.

Ready to wire qualified-stablecoin policies, sanctions hooks, and Travel Rule plumbing into your app? Start with the Openfort docs or pricing.