TL;DRAI agents are gaining the ability to spend money autonomously, and the teams that equip them with wallets unlock new revenue models, higher retention, and lower operational costs. This post walks through why agent wallets are strategic for product teams — not just a technical toggle. It covers when to give an agent its own wallet vs. share the user's, how to scope spend and policy, and what pricing and billing changes make sense once agents transact. Use it to frame the agent-wallet decision with your leadership. Read it before designing your agent's economic layer.

OpenAI shipped shopping inside ChatGPT in early 2026. Stripe and Tempo released the Machine Payments Protocol on March 18. Visa is on track for millions of AI-agent transactions by the 2026 holiday season. The rails are live. The question now is whether your product is set up to ride them, or whether your AI features still stop at recommendations.

The $3–5 Trillion Opportunity Product Teams Are Missing

McKinsey estimates AI agents will mediate $3–5 trillion of global consumer commerce by 2030, with US B2C retail alone in the trillion-dollar range. BCG puts the share of consumers already expecting to delegate shopping decisions to agents at 81%. Accenture has 57% of executives anticipating mainstream agentic payments within three years.

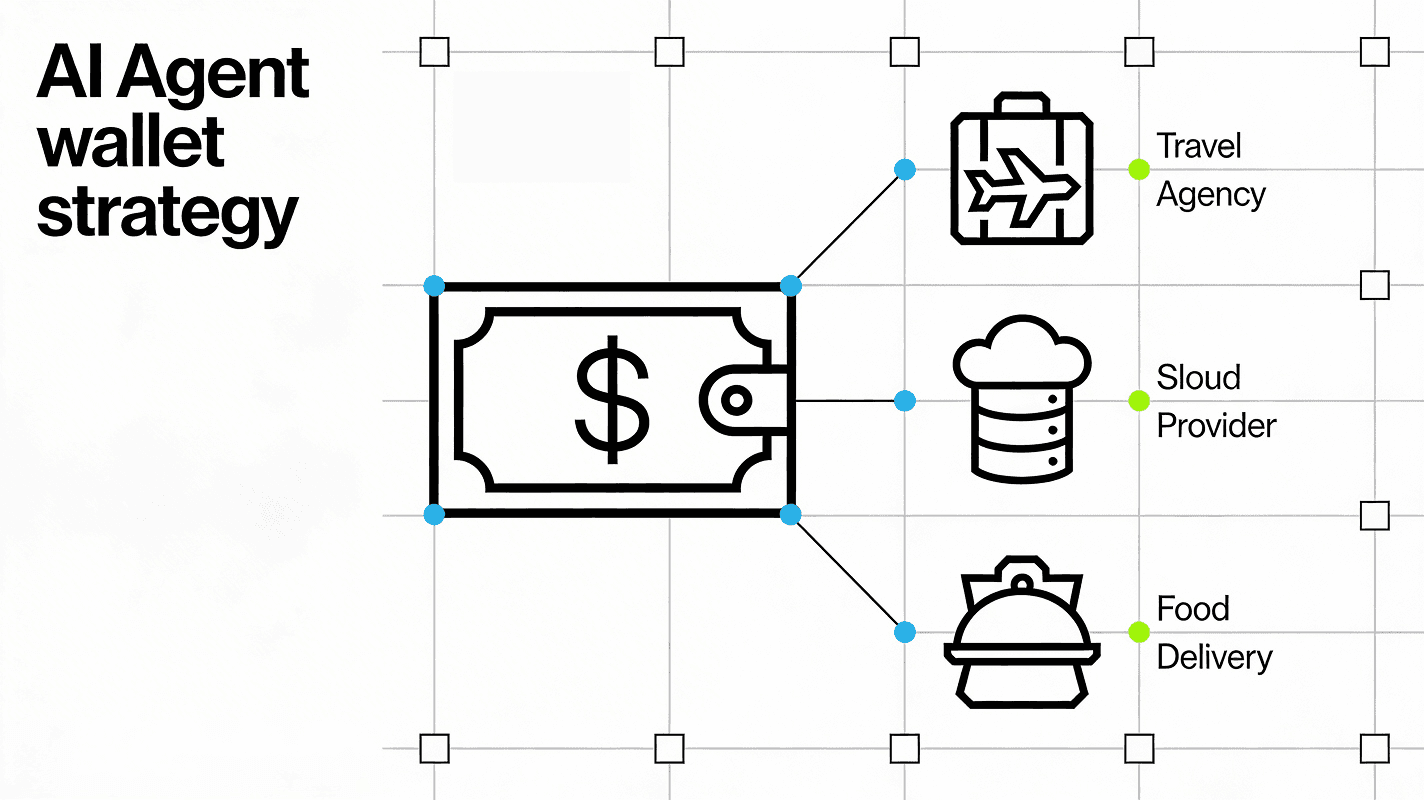

The shift behind those numbers is concrete. Agents are stepping past "give me an answer" into "go do it" — and "do it" usually means spend money on the user's behalf. The piece that turns an advisor into an executor is the wallet: a programmable account that holds funds, signs transactions, and operates within whatever guardrails you set.

That's what an AI agent wallet strategy means in practice. A deliberate plan for how your product's AI features touch money — what they can spend, where, and on whose authority.

What Happens When Your AI Assistant Can Pay

Four concrete scenarios, all blocked today by the missing wallet:

Autonomous procurement. An enterprise assistant watches inventory, finds the best price across vendors, and places a restock order — within a pre-approved budget, with no human in the loop until the goods arrive. For mid-market companies spending $2–10M a year on procurement, automating even a fifth of routine purchases pays for itself.

Subscription optimization. A personal finance agent reviews 14 SaaS subscriptions, kills the three you haven't used in 90 days, and reallocates the budget to a new tool — handling the cancellation flow, the refund, and the new sign-up from a wallet you fund with a monthly allowance.

Real-time service purchasing. A coding assistant hits a rate limit on a data API mid-task and buys additional credits via x402 — one HTTP request, settled in seconds. The user sees the result, not the transaction.

Cross-agent commerce. Your agent needs a contract review. It finds another agent that does legal analysis, agrees a per-page price, pays in stablecoin, and returns the annotated document. Agent-to-agent services become a new commerce layer with no human intermediary.

Each scenario has the same prerequisite: a wallet the agent controls, inside limits the product team defines.

Three Strategic Reasons to Act Now

1. User Retention Through Autonomous Features

Products that can act — not just advise — become harder to leave. When your AI assistant manages a user's recurring purchases, optimizes their spending, or handles procurement workflows, switching costs compound with every transaction.

This is the retention flywheel: an agent wallet transforms your AI from a tool into a service. Users delegate more over time. Each delegation deepens the relationship. Bain estimates that agentic commerce will reshape customer loyalty entirely, as the agent — not the brand — becomes the primary purchasing interface.

Product teams that wait will find their AI features commoditized. The assistant that can only suggest a purchase loses to the one that can complete it.

2. New Revenue Models

Agent wallets unlock business models that don't exist without them:

| Revenue Model | How It Works | Example |

|---|---|---|

| Agent-as-a-service | Charge users for autonomous purchasing capabilities | "Premium tier: your agent manages up to $5,000/month in purchases" |

| Transaction fees | Take a percentage of agent-initiated commerce | Marketplace where agents buy and sell data, compute, or services |

| Procurement automation | Charge enterprises for automated purchasing workflows | B2B platform where agents handle vendor selection and payment |

| Agent-to-agent services | Your agent sells capabilities to other agents | Legal review, data analysis, or content generation — priced per request |

These models share a common thread: they turn AI capabilities into revenue-generating services. Without a wallet, your AI is a cost center. With one, it can be a profit center.

3. Operational Cost Reduction

Manual purchasing workflows are expensive. Every purchase order that requires a human approval, every subscription renewal that needs a manager's sign-off, every vendor payment that routes through accounts payable — these are costs that compound.

Agent wallets don't eliminate oversight. They eliminate the routine. Configure spending limits, contract allowlists, and approval thresholds once. The agent handles everything within those boundaries autonomously. Humans review exceptions, not every transaction.

For companies processing thousands of routine purchases monthly, the math is straightforward: reduce the human touch points by 60–80% on transactions under a defined threshold, and redirect that labor toward strategic decisions.

The Product Decision Framework

Building an agent wallet strategy requires four decisions:

Decision 1: Custody Model

Who holds the keys?

- Custodial wallets are simpler but create liability. If you hold the keys, you're responsible for every transaction. Regulatory requirements (MiCA in Europe, state-level money transmitter laws in the US) may apply.

- Non-custodial wallets keep keys with the user or in a shared custody model. The product team configures policies, but no single party — including the provider — holds the complete key. This is the model most agentic commerce infrastructure is converging on.

For most product teams, non-custodial is the right default. It reduces regulatory exposure and aligns with the principle that users should control their funds — even when an agent acts on their behalf.

Decision 2: Control Granularity

What can the agent do?

The difference between a useful agent and a dangerous one is the control layer. Your strategy must define:

- Spending limits — per transaction, per day, per month

- Contract allowlists — which protocols and merchants the agent can interact with

- Session keys — temporary, scoped permissions that expire automatically

- Approval thresholds — transactions above a certain amount require human confirmation

- Kill switches — the ability to freeze agent activity instantly

These controls should be enforced at the infrastructure level, not in application code. Policies encoded in smart accounts are verifiable and tamper-resistant. Policies implemented as API middleware are bypassable.

Decision 3: Payment Rails

Which protocols will your agent support?

The protocol landscape is consolidating around four major approaches:

- Stripe ACP/MPP — fiat-native, works with existing Stripe merchants, backed by Stripe and OpenAI

- Google AP2 — identity and trust layer for agent-to-merchant interactions

- Coinbase x402 — crypto-native, HTTP-level payments, dominant in stablecoin transactions

- Visa TAP / Mastercard Agent Pay — card network approaches bridging existing merchant infrastructure

The right answer depends on your users and use case. A consumer product targeting mainstream users may start with Stripe MPP. A developer platform may need x402 for micropayments. An enterprise product may need all of the above. The most strategic approach is choosing infrastructure that is protocol-agnostic — so you're not locked into a single rail as the market evolves.

Decision 4: Build vs. Buy

How much infrastructure do you own?

Building agent wallet infrastructure from scratch requires deep expertise in key management, smart account architecture, gas optimization, and protocol integration. Most product teams should not do this. The build timeline is 6–12 months, and the maintenance burden is ongoing.

Instead, use purpose-built infrastructure. Openfort provides non-custodial agent wallets with programmable controls, session key management, and gas sponsorship out of the box. Integration takes minutes, not months — and you get the security guarantees (four independent audits, open-source key management via OpenSigner) without the engineering investment.

The strategic decision is where to invest your team's time: in wallet plumbing, or in the product features that differentiate you.

Getting Started: The 10-Minute Path

Openfort's SDK reduces agent wallet integration to a few steps:

- Create an agent wallet — a non-custodial smart account with its own address and signing capability.

- Configure session keys — grant the agent scoped permissions (which contracts it can call, how much it can spend, when the permission expires).

- Set up gas sponsorship — your users shouldn't think about gas fees. Openfort's policy engine lets you sponsor transactions by contract, function, or account.

- Connect to your agent framework — Openfort integrates with LangChain, CrewAI, and any framework that can make API calls.

The technical integration is deliberately simple so your team can focus on the strategic questions: what should your agent be allowed to buy? How much autonomy do users get to configure? What revenue model does this enable?

These are product decisions, not engineering problems. And the engineering work is the easier half.

What to do this quarter

The infrastructure is being built right now: Stripe MPP shipped March 18, OpenAI's shopping features are live, and Visa, Mastercard, Google, and Coinbase are all rolling out agent payment protocols. Teams that lock in their agent wallet strategy this quarter will be shipping autonomous features while competitors are still on whiteboards.

The decision points are the same four above — custody, control granularity, payment rails, build vs. buy. Pick a default for each, scope a small pilot (one workflow, one cohort, low spending limit), and ship it. The data you get from a real agent transacting against real users will sharpen every subsequent decision.

Ready to add wallet capabilities to your AI agents? Explore Openfort's agent wallet infrastructure or read the docs to get started in minutes.

Related Reading

- The Agentic Wallet Problem — the custody architecture behind agent wallets

- Agentic Commerce: Rewriting the Rules of Online Transactions — how AI agents are reshaping the commerce stack

- How x402 Works — the HTTP-native payment protocol for agent transactions

- How to Build an Agent Wallet — a step-by-step technical guide